Greenhouse Gas Reporting Coming Soon to Federal Contractors

Federal contractors who perform more than $7.5 million in total contracts in a single federal fiscal year may be subject to new greenhouse gas (GHG) inventory and reporting regulations.

The Biden administration released a proposed rule on Nov. 14, 2022, that would require federal contractors to disclose their GHG emissions and develop carbon reduction targets. This rule leverages the federal government’s buying power to directly affect climate change within the federal supply chain. Once finalized, the FAR Council will revise the Federal Acquisition Regulation (FAR) Part 9 (Contractor Responsibility), Part 12 (Commercial Products and Commercial Services), Part 23 (Environment, Energy, and Water Efficiency), and Part 52 (Provisions and Clauses).

Contractors and interested stakeholders may comment until Feb. 13, 2023, through the link above. The original comment was set to close on Jan. 13 but was extended to provide additional time for comment.

As proposed, the rule contemplates several new definitions and several new reporting requirements around GHG. For reference, GHG is carbon dioxide, methane, nitrous oxide, hydrofluorocarbons, perfluorocarbons, nitrogen trifluoride, and sulfur hexafluoride.

The proposed rule specifically divides contractors into three groups. To determine which group a contractor is in, it must calculate its total contract obligations in the previous federal fiscal year (Oct. 1–Sept. 30). From there, any contractor with less than $7.5 million in total contract obligations is not subject to the proposed rule. However, contractors above that threshold are subject to the proposed regulations and are then divided into two groups: “significant contractors“ with between $7.5 million to $50 million and “major contractors“ with more than $50 million. The proposed rule applies to both commercial and non-commercial products and services.

One year after the final rule is published, both significant and major contractors will be required to meet Scope 1 and Scope 2 reporting in the System for Award Management (SAM.gov). Two years after the final rule is published, major contractors will be required to meet Scope 3 and Science-based target initiatives to reduce their GHG emissions. The one and two year respective runways allow contractors time to familiarize themselves with the rules and the scope requirements before compliance is strictly required.

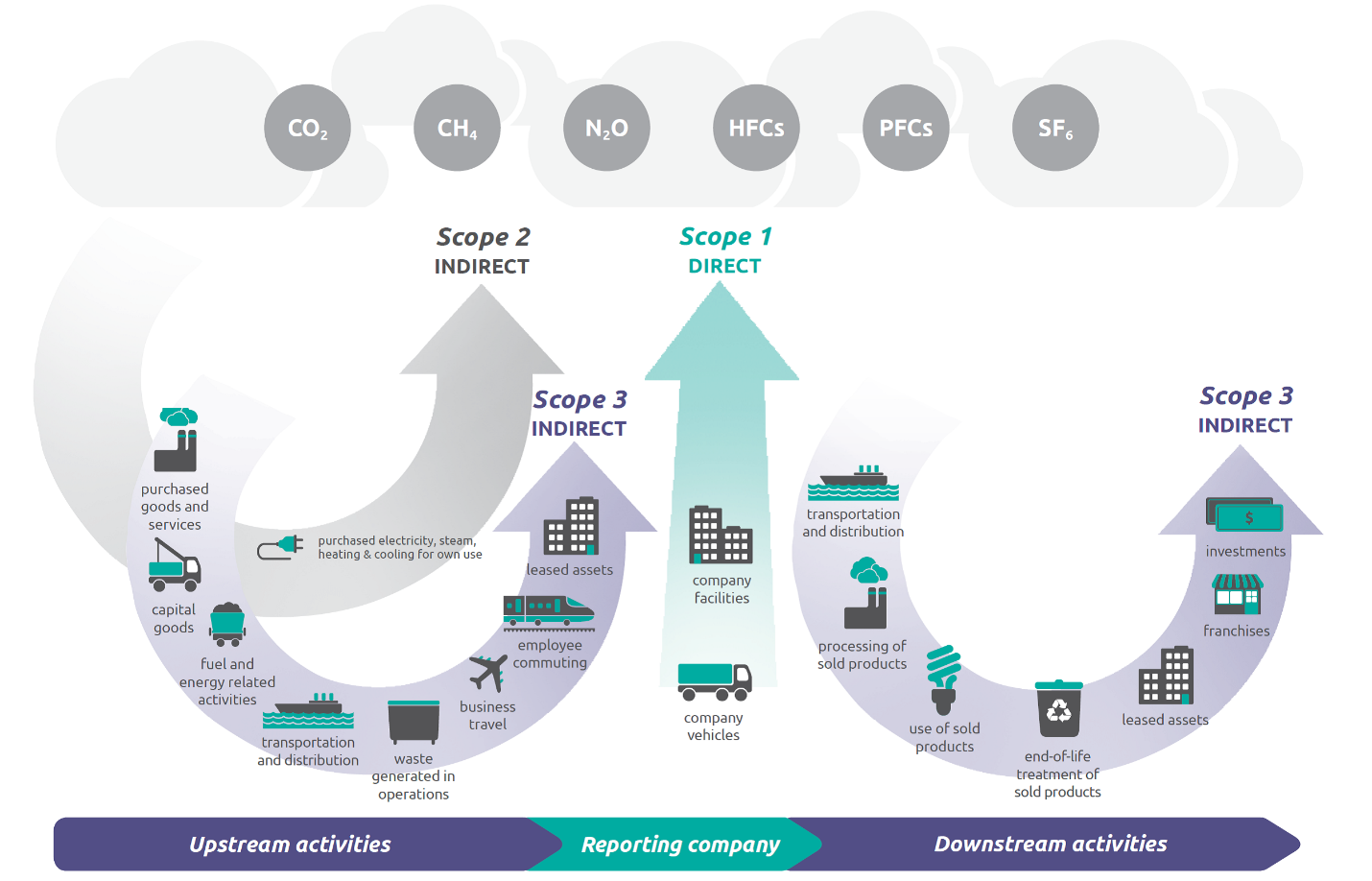

Scope 1 and Scope 2 will require significant and major contractors to take inventory of their GHG emissions, and Scope 3 will require an annual climate disclosure, along with progress toward science-based targets for emissions. Specifically, the proposed rule defines the scopes as follows:

- Scope 1 emissions mean direct GHG emissions from sources that are owned or controlled by the reporting entity.

- Scope 2 emissions mean indirect GHG emissions associated with the generation of electricity, heating and cooling, or steam when these are purchased or acquired for the reporting entity’s own consumption but occur at sources owned or controlled by another entity.

- Scope 3 emissions mean GHG emissions, other than those that are Scope 2 emissions, that are a consequence of the operations of the reporting entity but occur at sources other than those owned or controlled by the entity.

- Science-based target means a target for reducing GHG emissions that is in line with reductions that the latest climate science deems necessary to meet the goals of the Paris Agreement to limit global warming to well below 2°C above pre-industrial levels and pursue efforts to limit warming to 1.5°C (see SBTi frequently asked questions at https://sciencebasedtargets.org/?faqs#what-are-science-based-targets). For information on the latest climate science, see 2018 Intergovernmental Panel on Climate Change (IPCC) Special Report on 1.5°C at https://www.ipcc.ch/?sr15/?.

Greenhouse Gas Protocol, designer of widely used accounting tools to measure, manage, and report GHG emissions, developed the following infographic1 to further explain the differences between scopes:

There are a few exceptions: Alaska Native corporations, community development corporations, Indian tribes, Native Hawaiian organizations, Tribally-owned businesses, higher education institutions, nonprofit research entities, state and local government entities, or entities that have federal management and operations contracts that require similar reporting already. Further, entities that are exempt from SAM.gov registration under FAR 4.1105(a) are also exempt here.

Notably, small businesses are not exempt or excepted, because the government determined it would be most beneficial for small businesses and the government for them to participate in finding “opportunities to minimize climate risk in both their operations and their supply chains.”

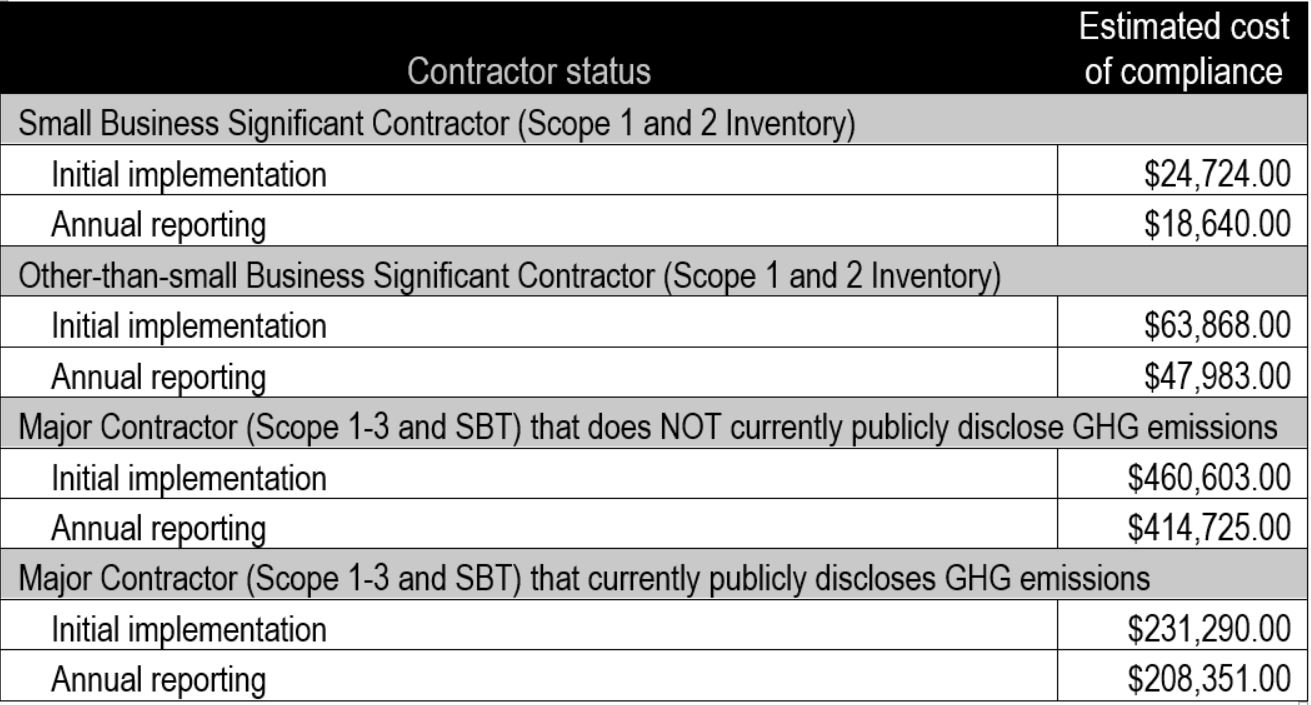

At present, the federal government anticipates the cost to implement and comply with the proposed rule will vary based on business size and current GHG reporting activity:

Companies that fail to respond as required may be determined “non-responsible“ under FAR 9.104-1, which in turn would negate their ability to be awarded a new contract award.

Interested parties may submit comments until Feb. 13, 2023.

In This Article

You May Also Like

DoW Review Pauses Parts of the CMMC Program Everything Old is New Again: Use of GSA Schedule Contract Vehicles on the Rise